Benefit in Kind Calculator (Download for Excel)

Use this one calculator to determine Class 1A and PAYE charges due on employee non-cash benefits in kind.

Get the Benefit in Kind Calculator (Excel Version)

To view how these values are calculated and compare tax years, enter your details and get the excel spreadsheet sent to you from ckp@tryzelt.com and reach out to info@zelt.app for any questions.

How benefits in kind are taxed

In most cases, benefits in kind are subject to income tax and employer national insurance contributions (NICs) in the same way as cash earnings except that employees do not pay NICs on BIK. You can use this NI contributions calculator to determine how much NI you pay.

Certain benefit in kind are exempt from NICs, HMRC gives specific guidance on tax treatment. To calculate how much taxes employees have to pay on BIK, first calculate the cash equivalent value of the BIK and then apply the employee’s income tax. On top of this, employers will need to pay NICs.

Employer NIC = BIK × 15%

Income Tax = BIK × 20/40/45%

When to pay taxes on BIKs

Taxes on benefits must be paid in one of the following two ways:

- At the end of the year

- Via payroll (MANDATORY from April 2027)

How to pay taxes on benefit in kind

Employers need to report the value of the benefit to HMRC, pay Class 1A employer NI contributions and deduct the appropriate amount of income tax from the employee’s pay. There are two possible way how to do this.

Payrolling benefits

You can add BIKs as non-cash income on employee payslips via a modern payroll system to automatically deduce income taxes from employees’ take home salary, and make NI contributions. But before you can do so you must registering with HMRC for payrolling benefits.

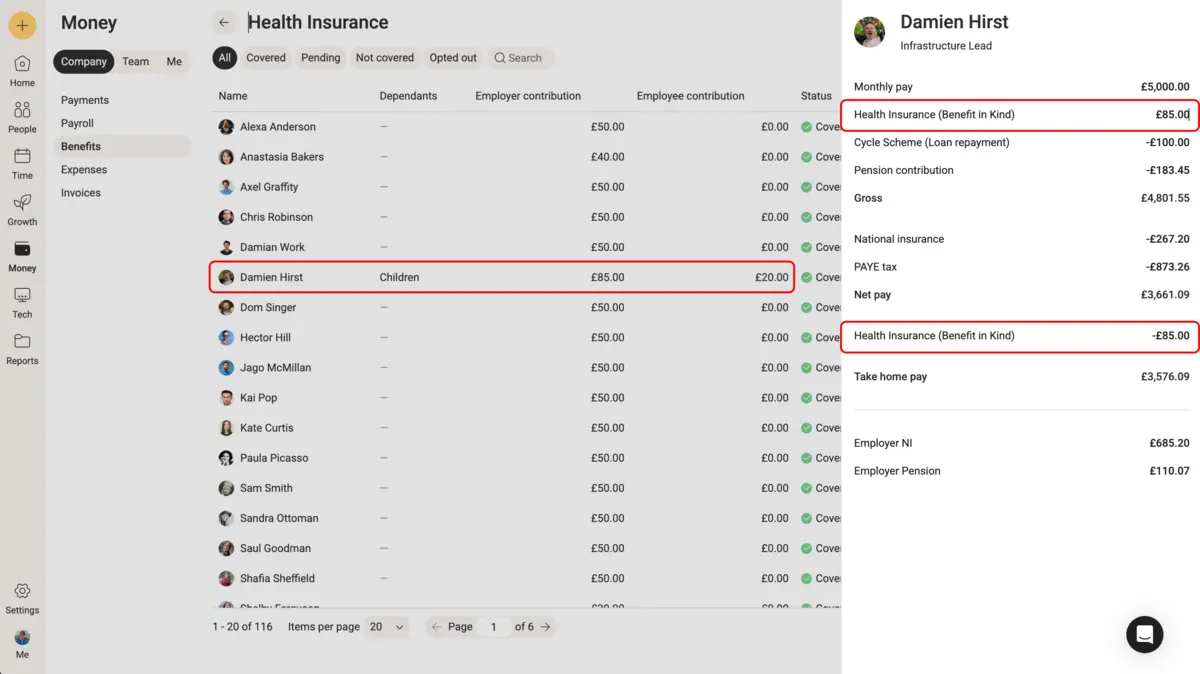

Example payslip with payrolled health insurnace

P11D form

In some cases, an employer may choose not to payroll a benefit in kind, either because the value of the benefit is small or because it is not practical to do so. In these cases, the employer is required to report the benefit to HMRC using a P11D form.

A P11D form is a tax return that is used to report benefits in kind that are not paid through the payroll system. It is typically completed by the employer and submitted to HMRC by the deadline of 6 July following the tax year in which the benefit was provided.

The P11D form must include the name and National Insurance number of the employee, as well as the type and value of the benefit in kind. The employer is also required to pay Class 1A NICs on the value of the benefit in kind, unless the benefit is exempt from NICs.

Manually calculating values for your annual filing can lead to errors and HMRC penalties. Use our P11D Calculator to instantly determine the reportable value and Class 1A National Insurance for your employees.

Introduction to RTI Reporting for Payrolled Benefits

From April 2027, HMRC requires reporting of all employee benefits in kind on employee payslips. With most companies running weekly or monthly payrolls, this is turning what was a once-a-year spreadsheet exercise into a real-time reporting challenge.

Book a seesion with one of our payroll specialists to run through what the new rules mean and how to prepare ahead of time by integrating your benefits offering with payroll.

Talk to an expert

Speak to us to learn how you can integrate your benefits offering with payroll.

What counts as a benefit in kind?

Benefits in kind can take many forms, such as company cars, private medical insurance, or free use of a gym on the company premises.

Some common benefit-in-kind items that are taxable in the UK include:

- Company cars

- Fuel provided for company cars

- Vouchers and credit cards

- Low-interest or interest-free loans

- Accommodation

- Non-business-related travel and accommodation

- Non-work related training

- Health screenings

- Gym memberships

- Loaning mobile phones and other electronic devices

Reporting benefits in kind

There are several ways to report BIK to HMRC. The most common method is through the payroll system, either as a separate amount or as part of the employee’s gross pay. You can also report BIK using the Employer Payment Summary (EPS), which is an online service provided by HMRC.

If you are reporting BIK through the payroll system, you will need to ensure that you are using the correct tax codes and that you are deducting the appropriate amount of tax and NICs from the employee’s pay. You will also need to keep accurate records of the BIK provided to your employees, including the value of the benefit and the date it was provided.

Using a Company Car Tax Calculator

The benefit in kind (BIK) tax on company cars is based on two main factors:

- The car’s CO2 emissions

- The car’s list price (also called P11D value)

BIK on company cars also depends on the type of fuel used. For example, diesel, petrol, electric, and hybrid cars all have different tax rates. Electric cars usually have lower rates. Tax rates may change each tax year.

You can save your time in calculating BIK value by providing company cars or fuel benefits using a company car tax calculator. This helps in avoiding the mistakes in tax calculations and ensures accurate reporting on payslips or P11D forms.

Frequently Asked Questions

What does benefit in kind mean?

Benefits in kind are non-cash benefits.

What are some examples of benefits in kind?

Some common examples of benefits in kind include company cars, private medical insurance, low-interest loans, company-provided accommodation, and gym memberships.

When are P11D forms due?

P11d forms must be submitted to HMRC by the 6th July following the end of the tax year.

How is benefit in kind tax calculated?

Employees pay income tax at the marginal tax rate, for example 20% if you earn below £50,000 annually and 40% of you earn £70,000 annually, and employers pay National Insurance contributions (Class 1A) at the rate of 15%.

How much is benefit in kind tax?

Employers pay 15% (Class 1A NI) and employees pay either 20%, 40% or 45% (income tax) depending on annual income